The Central American Economy Shows Resilience and Projects Growth Above 3% by Year’s End

Central America closed 2025 with an estimated GDP growth of 3.2%, underpinned by economic recovery indicators. This is reflected in data compiled by ADEN International Business School, whose regional estimate places growth above 3% by year-end.

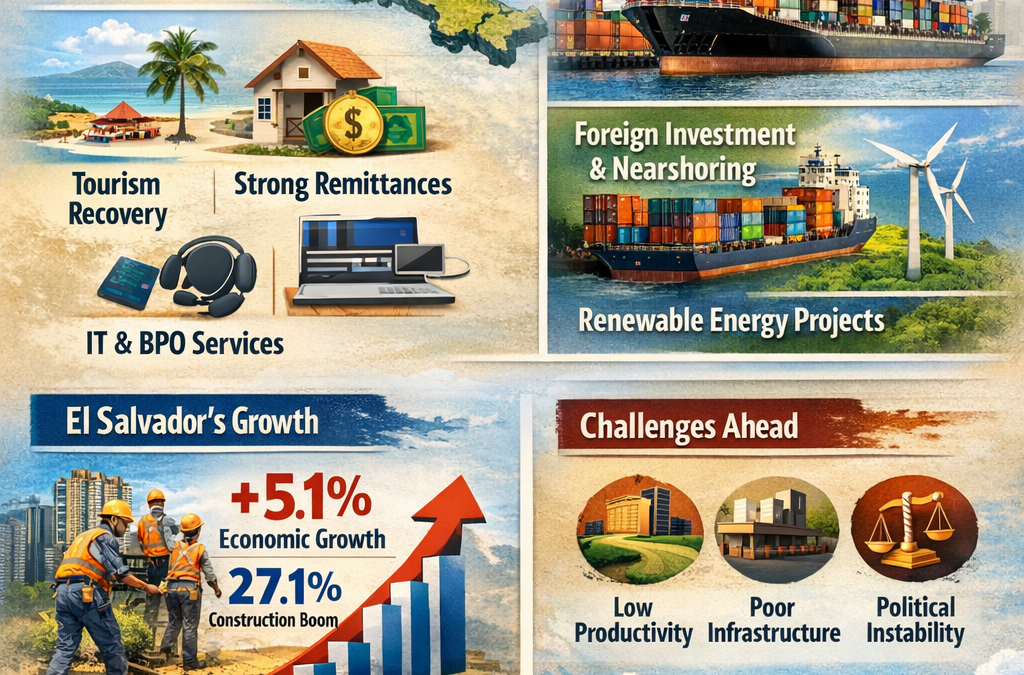

The organization points out that this projection takes into account the gradual normalization of tourism activities and remittances, as well as the strong pace presented by the services sector.

“Activity has been marked by high interest rates globally and continued volatility in supply chains,” says the report Economic Trends in the Central American Region and El Salvador 2025–2026. However, the Central American economy “has exhibited moderate resilience amid global market volatility.”

Likewise, the study highlights that the region closed 2025 by containing inflationary pressures recorded since the pandemic; thus, projections place this indicator in a year-on-year average rate of 2.6%.

El Salvador was one of the countries with the lowest inflation

For its part, inflation in the Central American economy of El Salvador stood out as one of the lowest rates in the region, with an annualized rate of 0.91%, a factor that benefits price stability and increases the confidence of investors and financial analysts.

Sources of Growth for Central America’s Economy

Regional growth is based mainly on “the services sector, the sustained recovery of tourism activity after the pandemic, and remittances,” report the consultants at ADEN Business School. These three factors “fuel domestic consumption” in countries where funds sent from abroad represent more than 20% of GDP, as in Guatemala, Honduras, and El Salvador.

Structural elements have favored the upward trend of the Central American economy, especially those economies that have been able to diversify their exports and expand their presence in foreign markets. The main ones are:

- Tourism has reopened strongly after the pandemic. This sector was impacted by restrictions on international travel but has recovered strongly, boosting economies such as Costa Rica, Panama, and the Dominican Republic.

- Remittances remain strong in Central America, especially those sent from the United States. These resources represent a substantial contribution to household income and therefore boost domestic demand.

- Business process outsourcing. Several Central American countries have managed to attract call centers and services for IT outsourcing. The industry has grown in the region and continues to offer new opportunities in digitization and support services.

ADEN analysts report that “tourism has been essential to reactivate SMEs after the health emergency.” Hotels, restaurants, taxi drivers, and tourist guides have experienced a gradual recovery, allowing companies in this sector to increase their payroll.

Technology services have also continued to grow in the region. Costa Rica, Panama, and El Salvador have managed to create specialized service platforms that offer services such as multilingual call centers, software development companies, and digital banking services to international clients.

Foreign investment finds a haven in Costa Rica and Panama

Costa Rica and Panama have been the countries most capable of attracting foreign investment to the Central American economy, mainly in technology and logistics projects. “The reconfiguration of global supply chains and geostrategic positioning” has become a determining factor in welcoming capital and projects with added value in both nations.

Multinationals have begun to include the region within the framework known as nearshoring. By this term, companies are referred to that seek to relocate their operations closer to North American territory, strengthening economies such as Costa Rica and Panama, which offer competitive labor and a stable legal framework.

Projects that have stood out in recent years include:

- Medical devices and specialized manufacturing.

- Logistics projects and warehousing close to the Panama Canal.

- Innovation centers and technology services.

- Projects related to renewable energies such as wind and solar farms, and geothermal.

Costa Rica, for example, has become a benchmark in attracting high-tech projects and medical device manufacturing. On the other hand, Panama continues to take advantage of its logistics capacity and project development next to the Panama Canal.

El Salvador bets on citizen security and digital transformation

On the other hand, El Salvador closed 2025 driven by two major government initiatives focused on citizen security and financial digitalization. Preliminary results published by the Central Reserve Bank (BCR) indicate that the Salvadoran economy grew 5.1% in the third quarter of 2025.

This growth was led by investment, both private and public, especially in the construction sector, which grew by 27.1% during the referenced quarter.

Other sectors that have helped the Salvadoran economy maintain annual growth are:

- Transportation services

- Administrative and support services

- Financial services

- Manufacturing industries

Government support and initiatives linked to public security and digital transformation have helped improve confidence among investors and the local population. Security, in particular, has been key to attracting visitors, real estate investment, and entrepreneurs.

Public debt, however, is one of the factors that must be monitored in the short and medium term. At the end of 2025, public debt reached 89% of GDP, “which should continue to be monitored in the short and medium term,” warns the central bank.

Structural challenges to improve in Central America

Central America is starting to grow, but the region still faces major structural challenges. Productivity levels, access to education, and infrastructure development are issues that set Central American countries apart from other emerging economies.

- A series of obstacles stand out among these challenges, including:

- Low labor productivity, especially in agriculture and traditional manufacturing.

- High levels of inequality between countries.

- Insufficient or deteriorated infrastructure, such as ports, roads, and energy plants.

Political instability affects growth and investment in countries such as Nicaragua and Honduras.

“In addition to growing,” points out Gustavo Riveros Sachica, director of ADEN’s Master’s in Strategic Development, “what we need to do is transform that growth into sustainable productivity and quality employment.”

Salvadoran authorities now have the opportunity to increase investment in sectors other than remittances. “It has a historic opportunity to attract long-term industrial projects because it already has stability and has improved its security perception.”

What does the future hold for Central America?

Forecasts for economic growth in Central America are favorable for the coming years. Expansion will be relatively flat but steady throughout the region.

The region will continue to rely heavily on domestic demand, but increased foreign investment and tourism will provide a fillip to growth rates.

Countries like Costa Rica, Panama and Honduras have the opportunity to continue developing their education systems, improve productivity, and attract investment in sectors such as technology, advanced manufacturing and logistics.

If successful, these reforms could convert Central America into a highly competitive region for investment and one of the main destinations for services, logistics projects and high-tech industries in Latin America.